When people think about credit scores, they often link them to loan approvals or credit card limits. But one lesser-known, yet significant, use of your credit score is in determining how much you pay for insurance. From auto to homeowners insurance, your credit behavior can quietly shape your premiums—and many don’t even realize it.

Understanding how and why your credit score affects your insurance rates is the first step in taking back control and saving money.

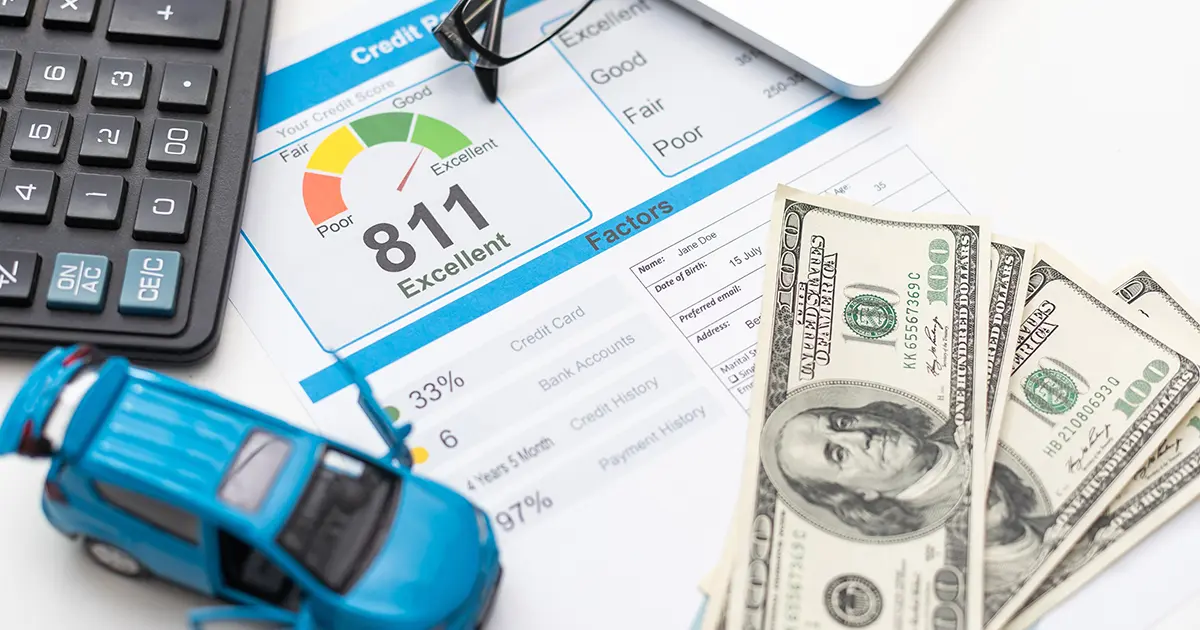

The Link Between Credit and Insurance

Insurance companies use a version of your credit score, often called a credit-based insurance score, to predict how likely you are to file a claim. Studies by insurers suggest that individuals with lower credit scores file more claims and cost more to insure. Based on this logic, those with higher scores are seen as less risky—and are rewarded with lower premiums.

This scoring model is not the same as your FICO or VantageScore used by lenders. Instead, insurers focus on certain credit behaviors, including:

-

Payment history

-

Debt-to-credit ratio

-

Length of credit history

-

Types of credit

-

Number of hard inquiries

They do not consider your income, race, marital status, or employment history.

How Credit Scores Affect Insurance Types

Here’s a breakdown of how your credit profile can influence different types of insurance:

| Insurance Type | Impact of Credit Score |

|---|---|

| Auto Insurance | Widely used in premium calculation in many U.S. states. Higher scores = lower premiums. |

| Home Insurance | Credit-based scores often used to assess homeowner risk. Can affect premiums significantly. |

| Renters Insurance | Some providers check credit before issuing a quote or policy. |

| Life Insurance | Less common, but some insurers may still consider your credit indirectly. |

In states like California, Hawaii, Maryland, Massachusetts, and Michigan, insurers are restricted or prohibited from using credit scores in pricing certain insurance products.

Also, check: Marine Insurance: Coverage for Shipping and Boating

Real-World Example

Consider two drivers with identical demographics and driving records:

-

Driver A has a credit score of 780

-

Driver B has a credit score of 600

Driver A might pay 30–50% less on auto insurance—even if both have never filed a claim. The difference lies purely in how insurers perceive financial responsibility through credit behavior.

Why Insurers Use Credit Scores

Insurance is all about risk prediction. Insurers argue that people with lower credit scores are statistically more likely to:

-

Miss premium payments

-

File more frequent or larger claims

-

Exhibit financially risky behavior

By pricing based on credit, insurers say they are better able to keep costs fair across all policyholders.

Controversies and Criticisms

Critics argue that credit-based insurance scoring is unfair, especially since:

-

It disproportionately affects lower-income communities

-

A person’s driving record or claims history should matter more than their credit card habits

-

Medical bills or one-time financial crises can damage credit despite responsible behavior

Consumer advocacy groups have pushed for greater transparency and limits on using credit in insurance pricing.

Tips to Improve Your Insurance Rates Through Credit

-

Pay bills on time – On-time payments make up a large portion of your score.

-

Reduce credit card balances – Lower utilization rates improve your profile.

-

Avoid unnecessary credit inquiries – Too many hard pulls can hurt your score.

-

Check your credit report regularly – Fix any errors or inaccuracies that could drag you down.

-

Ask your insurer about discounts – Some offer savings for improving your score or bundling policies.

Even small improvements in your credit can lead to noticeable drops in your insurance premiums over time.

Conclusion

While it may seem odd that your ability to manage credit affects your insurance costs, this is the reality in many parts of the world. Knowing the link between credit scores and insurance rates empowers you to make smarter financial decisions—not just for loans, but for protecting your assets too.

If you’re getting quotes or renewing a policy, it’s worth checking your credit and asking how it’s impacting your premium. In insurance, financial responsibility doesn’t just pay off—it pays less.